Small Business Loan vs Using Credit Cards: Pros, Costs & How to Decide in 2026

Photo by Tim Mossholder

At some point, most small business owners run into a moment where they’re in need of capital.

Most commonly, it can be for inventory during a busy season. Or equipment to finally let you scale beyond your current operations.

When this happens, the question which rises to the top is:

Do I take out a small business loan…or just use credit cards?

If you’re a parent building a side hustle after bedtime or a working professional testing your first real business idea, this decision feels bigger than it looks. Financing choices can either fuel your growth or quietly chip away at your margins.

I’ve worked with founders who swiped their way through growth and paid dearly in interest. I’ve also seen business owners take on loans that were larger than they needed and feel boxed in by fixed payments before revenue stabilized.

Both options can work. Both can backfire.

Capital is a tool when used wisely at it can accelerate growth. If used carelessly though, it can make matters much worse.

What Is a Small Business Loan?

A small business loan is exactly what it sounds like: you borrow a fixed amount of money upfront and agree to repay it over a set period of time, usually with interest.

You receive the funds in one lump sum. Then you make structured payments (often monthly) until the balance is paid off.

For many business owners, this feels more predictable than relying on credit cards. You know the payment. You know the timeline. You know when it will be done.

The Most Common Types of Small Business Loans

Not all business loans look the same. The structure depends on who’s lending and what you need the money for.

Here are the most common options:

#1: Term Loans

This is the classic model.

You borrow a specific amount and repay it over a fixed term (often 1–10 years).

Rates may be fixed or variable. These are commonly used for equipment purchases, expansions, hiring, or other growth investments.

#2: SBA Loans

Loans backed by the U.S. Small Business Administration are some of the most well-known options for small businesses.

The SBA doesn’t directly lend the money in most cases — instead, it guarantees a portion of the loan through approved lenders, which lowers risk for banks.

That guarantee often means:

Lower interest rates

Longer repayment terms

Larger loan amounts

The tradeoff is more paperwork and stricter qualification requirements. If you’re curious, you can explore official SBA loan programs directly on the SBA website.

#3: Online Lender Loans

These are typically faster to obtain and require less documentation.

Approval can happen quickly, sometimes within days. Interest rates may be higher than traditional bank or SBA-backed loans, but they can be helpful when timing matters.

Typical Loan Amounts and Terms

Small business loans can range anywhere from a few thousand dollars to several million, depending on the lender and your qualifications.

What lenders usually evaluate:

Your personal and business credit scores

Time in business

Revenue and profitability

Cash flow consistency

Existing debt obligations

If you’re early-stage or still validating your idea, qualifying can be more difficult. That’s why we always encourage founders to understand their numbers first.

If you haven’t yet dialed in profitability expectations, revisit my article on what is a reasonable profit margin for a small business?.

Financing works best when the business fundamentals are steady.

Why Business Owners Choose Loans

A loan makes sense when:

You need a larger amount of capital

The expense is long-term (equipment, buildout, acquisition)

You want predictable repayment

You’re confident the investment will generate steady returns

If you’re buying a $40,000 piece of equipment that will serve you for five years, spreading that cost over time through a structured loan often aligns better than putting it on a high-interest credit card.

That said, loans are not “easy money.” They require planning. Fixed payments don’t disappear during a slow month. And qualifying can take time.

A business loan is often a growth tool for established operations. For newer businesses or side hustles that are still stabilizing income, flexibility sometimes matters more than structure.

What Is a Business Credit Card?

If a small business loan feels structured and formal, a business credit card feels fast and flexible.

You’re approved for a credit limit. You can spend up to that limit. You repay what you borrow, and as you pay it down, that credit becomes available again.

That revolving structure is why so many entrepreneurs reach for credit cards first. They’re accessible. They’re familiar. And in many cases, they’re quick to open.

Speed matters when you’re building a business in between school drop-offs and Zoom calls.

How Business Credit Cards Work

A business credit card operates similarly to a personal card, but it’s designed for business expenses. You receive:

A revolving credit line

A minimum monthly payment requirement

An interest rate (APR) applied to any balance you carry

If you pay your balance in full each month, you avoid interest. If you carry a balance, interest accrues — often at rates significantly higher than most term loans.

Some business cards offer introductory 0% APR periods.

Those can be helpful if you’re disciplined and confident you’ll pay off the balance before the promo window closes. Once the promotional period ends, the standard APR applies to any remaining balance.

Why Business Owners Like Using Credit Cards

There are real advantages here:

#1: Speed and Accessibility

Approval can happen quickly.

There’s typically less paperwork than a loan.

For newer businesses without years of financial history, this can feel like the only viable option.

#2: Flexibility

You can use the card for small, ongoing expenses (ex. software subscriptions, marketing spend, travel, inventory) without taking out a new loan each time.

#3: Rewards and Perks

Many business credit cards offer cashback, travel points, or category bonuses.

If you’re already spending on ads, shipping, or equipment, rewards can add up.

#4: Cash Flow Buffer

When invoices are slow or revenue is uneven (which is common in early-stage businesses), a credit card can help bridge short gaps.

Where Credit Cards Get Risky

The flexibility is what makes credit cards helpful — and what makes them dangerous.

Interest rates on business credit cards often sit well above most small business loan rates. Carrying a balance month after month can quietly erode margins.

There’s also a psychological factor. Revolving credit can feel less serious than signing formal loan documents. Swiping for inventory or marketing doesn’t always register the same way as committing to a structured repayment schedule.

For many side hustlers and early entrepreneurs, credit cards become the first form of financing simply because they’re available. Sometimes that works beautifully. Sometimes it creates a cycle that’s hard to unwind.

Understanding how a business credit card behaves over time is critical before deciding whether it’s the right tool — or just the easiest one.

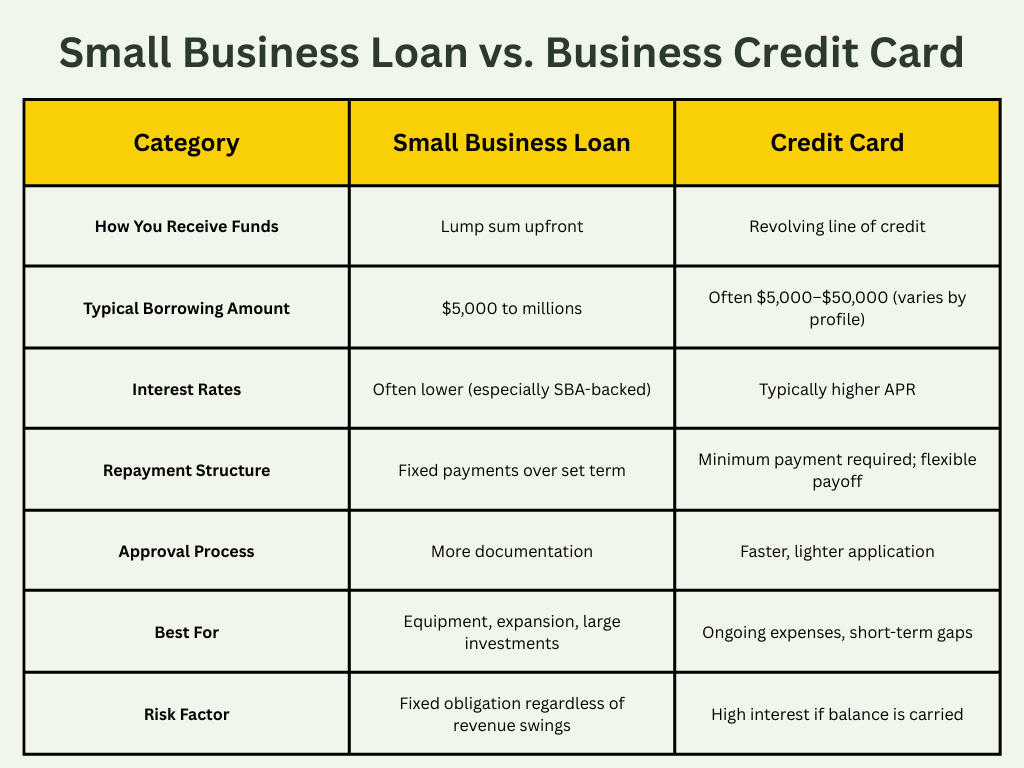

Small Business Loan vs. Business Credit Card: Side-by-Side Comparison

Once you understand how each option works on its own, the real clarity comes from putting them next to each other.

Most articles stop at surface-level pros and cons. What actually matters is how each choice affects your cash flow, stress level, and long-term profitability.

Here’s a clean comparison of small business loan vs business credit card across the factors that matter most:

Now let’s talk through what this actually means in real life.

Loan Structure: Predictable but Committed

With a loan, you know what you owe each month. That predictability can help you plan. It can also feel heavy if revenue slows down.

If you borrow $40,000 for equipment over five years, you’ll have a fixed payment whether sales are booming or not.

That structure works well when the investment directly supports stable, growing income.

This is why more established businesses often lean toward loans for major purchases. They can match the financing term to the lifespan of the asset.

Credit Cards: Flexible but Expensive If Carried

A business credit card gives you breathing room in the short term. You can scale spending up and down. You can pay more during strong months and less during slower ones.

The issue is compounding interest.

If you carry a $20,000 balance at a 20% APR, the interest alone becomes a real line item in your expenses. Over time, that cost quietly eats into margins.

When people search “when to use credit card vs loan small business,” this is usually what they’re trying to understand: the difference between short-term convenience and long-term cost.

Approval Reality

Loans, especially those connected to the U.S. Small Business Administration, require more documentation. Lenders will want to see revenue history, creditworthiness, and financial stability.

Credit cards are typically easier to obtain, especially if you have strong personal credit. Many early-stage founders rely on personal guarantees to qualify.

If your business is still in the “proving itself” phase, credit cards may be more accessible. As your revenue stabilizes, loans often become more attractive.

Cash Flow Impact

If your business has uneven revenue (common in service businesses, seasonal businesses, and new side hustles), flexibility may matter more than structure.

If your business has predictable monthly revenue, structured loan payments can feel manageable and even motivating.

Financing should fit the rhythm of your business.

Pros and Cons: An Honest Breakdown

Every financing option comes with tradeoffs.

Each financing option solves a different problem. The differences show up in your monthly cash flow, your stress level, and how much the capital ultimately costs you.

The goal is to understand how each one behaves inside a real business with real cash flow pressures.

Pros of a Small Business Loan

Lower total cost over time (in many cases)

Interest rates on term loans (especially those backed by the U.S. Small Business Administration) are often lower than credit card APRs.

When you’re borrowing a meaningful amount, that difference compounds in your favor.

Higher borrowing capacity

If you need $30,000, $75,000, or more for equipment, expansion, or hiring, loans are built for that scale.

Credit cards typically can’t support that level of capital.

Predictable repayment structure

Fixed monthly payments help you plan.

For businesses with steady revenue, this can reduce uncertainty because you know exactly what leaves your account each month.

Better alignment for long-term assets

Financing a five-year piece of equipment with a multi-year loan aligns the cost with the useful life of the asset.

That keeps your financing decision grounded in practicality.

Cons of a Small Business Loan

Harder to qualify

Lenders want documentation, revenue history, and credit strength.

If your business is still new or inconsistent, approval can be difficult.

Slower funding process

Loans take time.

If you need capital quickly, the timeline can feel frustrating.

Fixed obligation regardless of revenue swings

That payment is due whether it’s your strongest month or your slowest one.

For businesses with uneven cash flow, this lack of flexibility can create pressure.

Pros of Using a Business Credit Card

Fast and accessible

Approval is typically quicker and requires less paperwork.

For newer businesses, this accessibility can be critical.

Flexible repayment

You can pay down aggressively during strong months and scale back during slower ones, as long as you meet the minimum requirement.

Useful for recurring operating expenses

Marketing spend, subscriptions, travel, inventory restocks — credit cards handle these well.

Rewards and cashback potential

If you’re paying balances in full, rewards can offset real operating costs.

Cons of Using a Business Credit Card

Higher interest rates

Carrying a balance long term often costs significantly more than a term loan.

Margin erosion

If your profit margins are thin, high APR debt can chip away at them faster than you expect. What looks manageable at first can quietly reduce the money you’re actually keeping.

Before leaning heavily on credit cards, take a clear look at your margins and cash flow.

Financing decisions land very differently in a business with healthy cushion versus one running tight.

Easier to accumulate debt gradually

Revolving credit doesn’t feel as formal as signing loan documents.

That psychological difference can make it easier to let balances build quietly.

When It Makes Sense to Use Both A Small Business Loan and A Credit Card

This isn’t always an either-or decision.

Many healthy businesses use a combination of structured debt and flexible credit. The key is being intentional about which tool is used for which purpose.

A common pattern looks like this:

A term loan funds a long-term asset.

A credit card handles short-term operating expenses.

The structure of the financing matches the nature of the expense.

Match the Tool to the Timeline

Long-term investment? Long-term financing often makes sense.

Short-term expense? Short-term credit can work — as long as there’s a clear payoff plan.

If you’re purchasing equipment that will generate revenue for five years, spreading that cost across several years through a loan keeps your monthly cash flow manageable.

If you’re covering ad spend for a campaign that pays back within 30–60 days, a credit card can act as a bridge…especially if you pay it off quickly.

The danger comes when short-term debt becomes long-term debt. That’s usually how credit cards become expensive.

Using a Credit Card Strategically (Without Letting It Run the Show)

Credit cards work well when:

You pay the balance in full regularly

You’re using rewards to offset real expenses

You treat the credit limit as a ceiling, not a target

They become risky when balances quietly roll month to month without a defined repayment timeline.

If you’re considering this hybrid approach, decide in advance:

Which expenses go on the card

What your payoff window is

At what balance you stop charging

This kind of structure prevents drift.

Using a Loan Without Overextending

Loans also require guardrails.

Just because you’re approved for $100,000 doesn’t mean you should take $100,000. Borrow against projected revenue carefully and conservatively.

If you’re still validating growth or dialing in profitability, it’s worth strengthening your fundamentals before layering on structured debt.

The Quiet Advantage of Blended Financing

When used intentionally, a blended approach can:

Protect cash flow

Reduce overall interest costs

Provide flexibility during growth

Prevent overreliance on high-APR debt

Access to capital matters. Maintaining control over how and when you use it matters even more.

How to Decide Between a Small Business Loan and a Credit Card

As you think through which route to take, consider these five questions:

#1: How Stable Is Your Revenue?

If your revenue is consistent month to month, a fixed loan payment may feel manageable.

If revenue fluctuates (which is extremely common) flexibility might matter more.

Financing should match the rhythm of your income. When those two are out of sync, stress usually follows.

#2: How Long Will the Investment Pay You Back?

Think about the lifespan of what you’re funding.

Equipment that produces revenue for years

A buildout you’ll use long term

Hiring that supports sustained growth

Those are longer-term investments. Spreading that cost over time often makes practical sense.

Short-term expenses like marketing campaigns or inventory that turns quickly require a different lens. If the return happens fast and you have a clear payoff plan, short-term credit can work.

The repayment timeline should make sense relative to the payoff timeline.

3. What Does the Total Cost Look Like?

Look beyond the monthly payment.

Run the numbers on:

Total interest paid over time

APR differences

Fees

Promotional rates that eventually expire

A lower monthly payment isn’t always cheaper in the long run. Understanding total cost gives you clarity.

If margins are healthy and predictable, you have more room to maneuver. If margins are tight, even small interest differences can compound quickly.

4. What Is Your Exit Plan for the Debt?

Before you borrow, decide how it gets paid off.

Is it tied to a specific revenue stream?

Is there a defined payoff window?

What happens if revenue slows?

Debt becomes risky when there’s no defined plan for eliminating it.

5. How Much Risk Can You Comfortably Carry?

Every business decision also affects your household.

If you’re building a side hustle while supporting a family, your risk tolerance may look different than someone operating with no dependents.

That doesn’t mean avoiding growth. It means aligning financing with the broader life you’re building.

When people compare small business loan vs using credit cards, they’re often trying to reduce uncertainty.

The truth is that both tools can support growth when used deliberately. The right choice depends less on the product itself and more on your revenue stability, margins, discipline, and timeline.

Small Business Loan vs Using Credit Cards: The Bottom Line

Financing decisions shape more than your balance sheet. They influence how your business feels month to month and how much flexibility you have when revenue shifts.

A small business loan brings structure. It can work well when revenue is steady and the investment supports long-term growth.

A business credit card brings flexibility. It can smooth cash flow and cover ongoing expenses, especially when balances are paid down consistently.

Neither option is automatically right or wrong.

The decision comes down to whether the financing fits your business and your life. The repayment timeline should make sense relative to when the investment pays you back.

The structure of the debt should match the rhythm of your revenue. And the level of risk should feel manageable given your broader household responsibilities.

Before choosing, take time to run the numbers. Look at total interest over the full repayment period. Consider how a slower month would affect your ability to make payments.

Decide in advance how the debt will be eliminated.

Strong businesses use capital deliberately. Growth is far more sustainable when financing supports momentum rather than creating strain.

Frequently Asked Questions

-

It depends on how much you need, how quickly you need it, and how stable your revenue is.

A small business loan often makes sense for larger, long-term investments like equipment, buildouts, or hiring.

Credit cards can work well for short-term expenses or managing cash flow gaps, especially when balances are paid off quickly.

The better option is the one that aligns with your repayment ability and timeline.

-

Credit cards are often useful for:

Recurring operating expenses

Short-term marketing campaigns

Inventory that turns quickly

Bridging short invoice gaps

They work best when you have a clear payoff plan and avoid carrying high-interest balances long term.

-

In many cases, yes.

Term loans (especially those backed by the U.S. Small Business Administration) often have lower interest rates than business credit cards.

Over time, that difference can significantly reduce total interest paid.

However, loans may include fees and require longer approval processes, so the total cost should always be evaluated carefully.

-

Yes, many healthy businesses use both strategically.

A loan can fund long-term investments while a credit card handles day-to-day operating expenses.

The key is being intentional about which expenses go where and having a clear repayment plan for each.

-

It can help or hurt, depending on how it’s managed.

Paying balances on time and keeping utilization low can strengthen your credit profile. Carrying high balances or missing payments can have the opposite effect.

Discipline matters more than the tool itself.

-

The biggest risk is long-term high-interest debt.

If balances roll month to month without a defined payoff timeline, interest compounds and can reduce profitability. This is especially challenging for businesses operating with thin margins.

-

The primary risk is committing to fixed payments without stable revenue to support them.

If cash flow slows and the payment remains the same, pressure builds quickly. That’s why aligning repayment structure with revenue stability is so important.